Published August 25, 2025

San Mateo County Market Update - August 2025

%20(1).png)

What You Really Need To Know Before Buying a Home: Credit, Loans, and Costs

If you’ve been thinking about buying a home but feel overwhelmed by all the financial unknowns—you’re not alone.

Credit scores, loan types, down payments, closing costs, insurance… the list can feel endless. And if you’ve ever heard that you need a perfect credit score or 20% down just to qualify, you might be thinking homeownership is out of reach.

Let’s bust that myth right now.

In reality, you don’t need to have it all figured out before you start. You just need a clear understanding of your options—and the right guide to help you get there.

Here are the three big financial pillars every buyer should understand before jumping in.

1. Your Credit Score (and Why It’s Not Everything)

Credit scores do matter. But they’re not the full story—and you definitely don’t need an 800+ to buy a home.

Here’s a quick breakdown of what lenders typically look for:

-

Conventional loan: 620+

-

FHA loan: as low as 580 (with 3.5% down)

-

VA loan: no minimum score required by the VA (though many lenders prefer 620+)

The higher your score, the better your interest rate and monthly payment are likely to be. But lenders also look at your income, savings, debt-to-income ratio, and other factors—so a less-than-perfect score won’t necessarily disqualify you.

Pro tip: If your score needs work, you don’t have to pause your plans. A good agent and lender can help you make a game plan that gets you ready to buy—even if that means starting with a smaller goal or longer timeline.

2. Down Payments & Loan Options (Good News Ahead)

Let’s clear this up once and for all: You do not need a 20% down payment to buy a home.

Yes, putting down 20% helps you avoid PMI (private mortgage insurance), but there are many loan programs designed to help first-time and qualified buyers get into a home with less money upfront:

-

FHA loans: 3.5% down

-

Conventional loans: as low as 3% down for some buyers

-

VA loans: 0% down for eligible veterans

-

Down payment assistance: Available in many areas and often overlooked

Choosing the right loan type depends on your financial profile and long-term goals. A good lender (connected to the right agent!) will help you compare options based on what you qualify for and what works best for you.

3. The “Other” Costs You’ll Want to Plan For

Beyond the down payment, you’ll want to be prepared for a few other key expenses:

Closing Costs: These typically run 2–5% of the purchase price and include things like loan origination fees, appraisal, title insurance, and escrow.

Homeowners Insurance: In California, this one is worth calling out: the home insurance market is extremely tight right now, and costs are rising in many high-risk areas. Your lender will require coverage, so it’s important to get quotes early—especially if you're shopping in a fire zone or hillside community.

Other Potential Costs: Depending on your loan and down payment, you may also have monthly PMI. Property taxes, HOA fees, and future maintenance should also be factored in.

You Don’t Need to Be Perfect—You Just Need a Plan

The truth is, you don’t need to have perfect credit or a huge savings account to buy a home. What you do need is clarity, guidance, and a team that knows how to navigate the process step by step.

And that’s where I come in.

Think of me as your financial GPS—someone who understands your goals, connects you with trusted lending partners, and walks with you from “I wonder if I can buy” to “We got the keys.”

Whether you’re ready to jump in or just want to understand what’s possible, I'm here to help you build a smart, sustainable strategy.

Thinking of making a move? Let’s talk strategy.

Whether you’re buying, selling, or just exploring your options, I'm here to help you navigate the market with confidence.Let’s connect and talk about how homeownership can benefit you in today’s market! Email me at kevin@pickettrealestategroup.com or call me at 415.283.7919

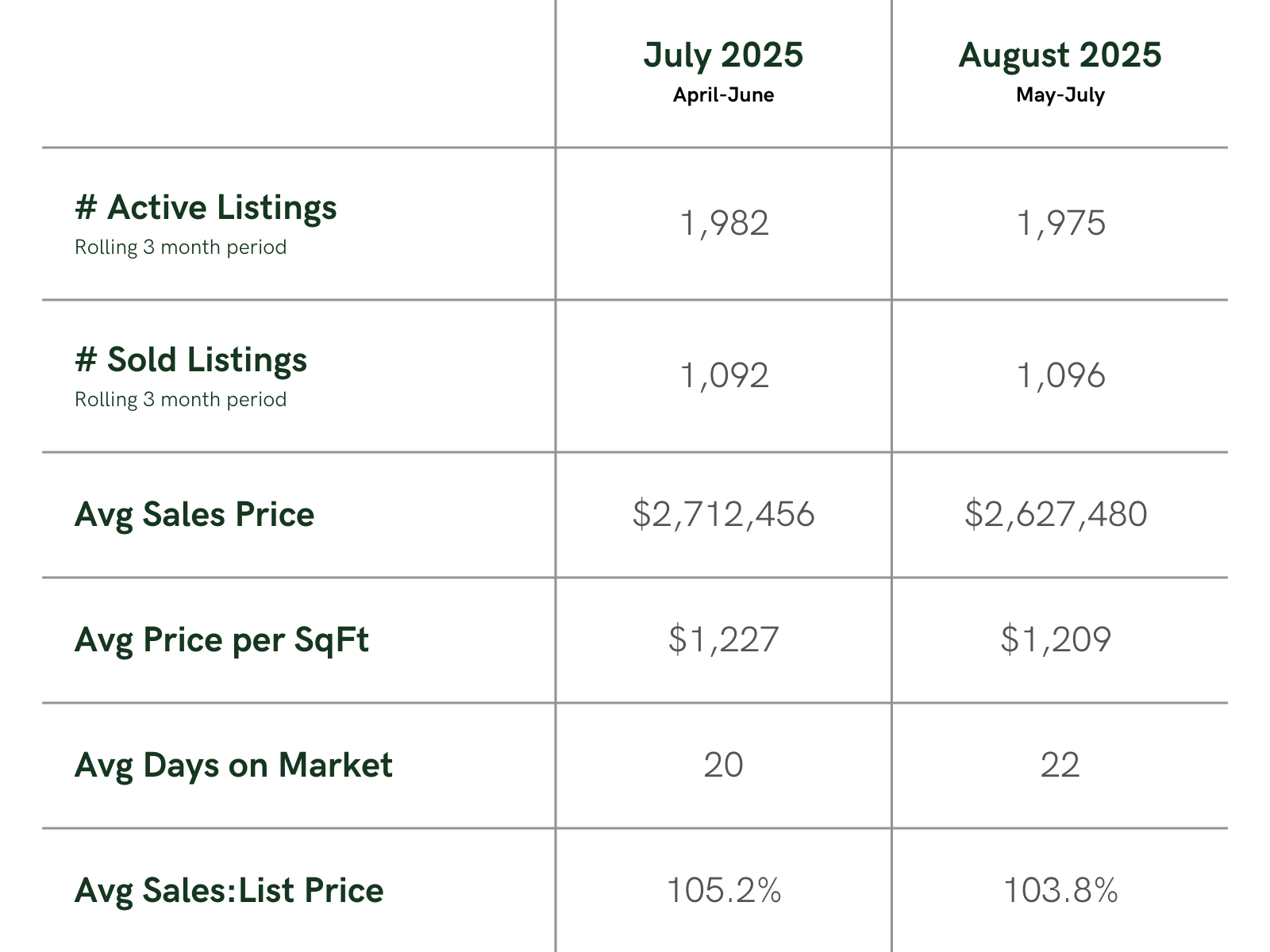

San Mateo County Rolling 3-Month Data

Below, our data is based on averages for Single-family homes in San Mateo County over the last 90 days (May 2025 to July 2025). This data was gathered on August 01, 2025.

San Mateo County Market Report

Thinking of selling?

I'd love to discuss your home's value and positioning in the current market. Call or text Kevin at 415.283.7919 or email Kevin at Kevin@PickettRealEstateGroup.com